The best accounting software in Switzerland

Whether you are a freelancer, entrepreneur, or small business owner, this article offers an overview of the top... En lire plus

The end of the accounting year in Switzerland is a time to ensure accurate and reliable financial reporting.

This process involves a number of steps that guarantee all accounting documents are recorded within the relevant period, providing unit and fund managers with up-to-date information.

Adhering to accounting standards such as Swiss GAAP FER and IFRS, and understanding the importance of assets and liabilities on the balance sheet, are essential for maintaining financial stability and transparency.

This article explores the key aspects of closing an accounting year, the significance of accounting standards, and the critical role of the balance sheet in reflecting a company’s financial health.

Switzerland follows two main accounting standards: Swiss GAAP FER and IFRS. Additionally, commercial bookkeeping and accounting are regulated by the Swiss Code of Obligations.

Financial Stability and Liquidity: The balance sheet reveals a company’s financial stability and liquidity. A balance of current assets and liabilities is crucial for liquidity, indicating the company’s ability to meet short-term obligations.

Asset and Capital Structure: The balance sheet shows how a company finances its assets. A high equity ratio suggests financial soundness, while a high debt ratio may indicate higher risk.

Leverage Effect: This describes the ratio of debt to equity. High debt levels can increase company risk due to interest and repayment obligations and also lead to higher returns for equity investors if investments are successful.

Overall Importance of Assets and Liabilities on the Balance Sheet

Assets and liabilities on the balance sheet provide crucial insights into a company’s financial health and stability in Switzerland. Understanding the various types of assets and liabilities, and their valuation principles, enables companies, investors, and other stakeholders to make well-informed decisions.

Compliance with legal regulations and accounting standards is essential for ensuring the transparency and comparability of balance sheets. Business owners must manage their accounting diligently and accurately value their assets and liabilities to present a true picture of their financial performance and stability.

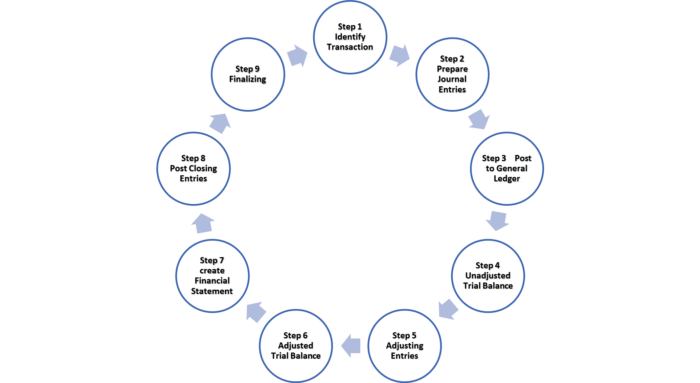

Accounting closure ensures the accurate recording of all financial documents within a specified period, providing reliable and up-to-date information for unit and fund managers. Let’s delve into the key aspects of closing accounts in Switzerland:

Before finalizing the accounting process, several critical operations with fiscal implications must be carried out. Let’s explore these key steps:

The inventory account needs to be adapted. This involves reconciling physical stock with recorded values to ensure accuracy.

Transactions related to asset depreciation (such as machinery, equipment, or vehicles) must be entered. Depreciation affects the company’s financial statements and tax liability.

Assess any transitional income or liabilities that impact the financial position during the transition from one accounting period to another.

Complete the Value Added Tax (VAT) declaration. Accurate VAT reporting is crucial for compliance and managing tax obligations.

Determine how to allocate the profit or loss. This decision affects tax liability and financial reporting.

Consult with your tax advisor or accountant to make informed choices based on your circumstances.

Conduct thorough verification and checking of all financial data. Accuracy is essential for compliance and reliable reporting.

Keep in mind that while the program may not distinguish between high and low profits, fiscal implications can greatly affect your financial standing. Seeking advice from a specialist, particularly if you’re new to managing accounting, can offer valuable insights. Accountants tend to be very busy during tax declaration periods, so it is wise to meet with them or share your accounting files well before closing the books. The eventual distribution of profits to shareholders will depend on the company’s structure (e.g., SA, SARL, etc.).

The closing process is vital in accounting as it prepares a company for the next accounting period by clearing any outstanding balances in specific accounts that should not carry over. This process involves returning these accounts to a zero balance.

The primary goals of the closing process are to:

Monitoring the closing balance at the end of each accounting period is crucial. It indicates whether a business is overspending or not generating enough revenue. A negative closing balance signals the need for changes.

Closing entries affect the profit and loss of a business only within a specified reporting period, typically a month, quarter, or year. These entries are reported on the income statement for that period. Other transactions may have more long-term effects on the business.

In conclusion, closing an accounting year in Switzerland is a meticulous process that ensures the accuracy and reliability of financial reports. By adhering to established accounting standards and carefully managing assets and liabilities, companies can provide a transparent and accurate picture of their financial performance.

This not only aids in compliance with legal regulations but also supports informed decision-making by stakeholders.

Understanding the accounting cycle, particularly the closing process, is vital for maintaining financial stability and preparing for future financial periods. Business owners and accountants must work diligently to ensure that all financial activities are accurately summarized and reported, fostering trust and confidence among investors and other stakeholders.

By the same author:

VAT in Switzerland: Implications and Insights

The best accounting software in Switzerland

Sources: SECO, Dates for closing accounts

Images: depositphotos