Eight H&S Strategies to Improve Performance

Have you engineered all your #health & #safety risks to acceptable levels? Are you still seeing avoidable incidents?... En lire plus

Organisational Health, Safety and Environment (HSE) is concerned with the management of related legal, economic, social, and ethical (LESE) risks and opportunities.

How these “LESE” drivers are viewed and prioritised within an organisation as a whole provides one of the clearest means of identifying its true HSE Type even if the business has not consciously selected the latter. The goal, however, should be for organisations to choose their type before developing an HSE strategy.

I believe there are considerable business and HSE benefits—not to mention avoided harm to people and the environmental—to doing this.

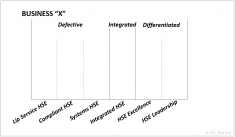

I divide organisational HSE management into three categories: defective, integrated, and differentiated. Within these groupings are six HSE Types that represent the organisation’s chosen HSE aspirations or its inherent bias. In the case of the former, the HSE strategy and mission are then built to deliver on the preferred target.

The conscious selection of its HSE Type and the resultant business benefits differentiates this approach from the ever-progressing and outdated HSE maturity model.

The basic model, right, shows the three HSE Categories (top) subdivided into the six HSE Types (bottom) as detailed in a previous article.

The basic model, right, shows the three HSE Categories (top) subdivided into the six HSE Types (bottom) as detailed in a previous article.

An organisation selects its Type, and then works to achieve this. There is no stepwise movement rightwards along the x-axis. Only notable business change or review would result in a new HSE Type being targeted; the HSE strategy would then be reworked to ensure it remains fit-for-purpose.

The goal is to rapidly achieve the chosen HSE Type. Therefore, there is less focus on characterising progression, and more on tracking and completing the projects and programmes the organisation views as essential to its vision of success.

One of the goals of the HSE Types model is for businesses to understand upfront the HSE resourcing requirements (costs) necessary to achieve their chosen HSE Type.

This, in turn, helps the business to plan, budget, and communicate clearly from the start the direction in which all employees must pull. It also helps HSE by right-sizing the function from the outset, giving them a clear operational scope and mandate, and avoiding later what the business might interpret as scope or budget creep as the team tries to fulfil a less business-transparent (but however valid) goal.

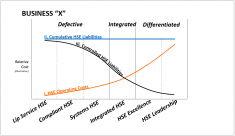

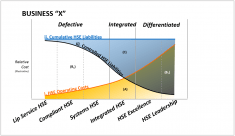

Because of the economics involved in organisational HSE management, each HSE Type has a distinctive relationship between its relative operating cost, liabilities, and cost-avoidance (see graph below).

Author’s note: due to difficulties in obtaining and publishing company-sensitive, real-world HSE data, all graphs are for illustrative purposes only.

This line represents the relative size of the organisation’s HSE budget (and effort).

This line represents the relative size of the organisation’s HSE budget (and effort).

Because defective HSE Types only view the function as a business cost, they will minimize budget and effort. Therefore, Lip Service HSE will cost the company next to nothing, followed by Compliant and the paper-based Systems HSE. This, however, comes at a cost (discussed in the following sections).

Integrated HSE will cost comparatively more given its deeper involvement in business activities. Achieving HSE Excellence or Leadership will require even greater operational investment, commitment, and effort from the business. Each HSE Type, however, will view its relative HSE operating cost favourably compared to the other Types.

Even when one is not actively targeted, internal profit-and-loss “market forces” within the business will likely drive HSE to a specific type. Depending on personnel efforts, the final Type may be marginally better or worse than what the HSE budget would predict—it will also be unsustainable (good people will leave or risk burning out, or “bad eggs” will be sacked).

This is the sum of all business HSE-related risks reduced to a monetary and accounting value.

A snapshot of any company’s activities will reveal a particular LESE risk profile independent of the HSE Type (chosen or otherwise). What the Type changes is how the business responds to and manages those risks, and herein lies the potential wider business benefit or risk of a given HSE Type.

Some HSE risks will be known; significant ones may be recorded on the ledger as contingent liabilities. Operations will be expected to prioritise and eliminate or control all known risks over time. There will also be unknown liabilities—hidden because they’ve not yet been identified, or will occur as a surprise to the business and may have secondary (compounded) cost-to-company.

The ratio of known to unknown HSE liabilities is determined by the organisation’s effective HSE Type—the effort put into identifying risks before they occur. If top management identifies with the saying “no surprises”, then the principle of proactively identifying HSE risks should resonate. It should go without saying that businesses should seek to identify and minimise unknown risks or outcomes.

(I believe this last point, which drives businesses to assess long-term threats to operations and profit, is the business success of wider ESG (Environmental, Social, and Governance) disclosures such as CDP, DJSI, FTSE4Good, and GRI-G4.)

The magnitude of HSE (and other) risks are typically linked to a business’ activities or sector. Because of this and the fact that the Types model is a snapshot in time, line (ii) is flat. This might suggest the line is unimportant, but this couldn’t be further from the truth…

The potential costs-to-company that have been eliminated or mitigated as much as possible. HSE works to avoid LESE-related costs-to-company that affect people and the environment. How effectively it does this is linked to the organisation’s HSE Type, and thus changes across the model.

It should be obvious that defective HSE will fall short of all-but-superficially addressing its most visible HSE issues. This liability curve will be invisible to this group because, by definition, defective HSE Types don’t view HSE as cost-prevention. Defective HSE is, anyway, incapable of identifying the majority of its business HSE risks and so ignorantly risk-assesses based on incomplete data.

Integrated HSE fares better with far fewer “failures”. This is why it is a satisfactory target for most organisations, especially small-medium enterprises with real-world budget constraints offset by a positive will to manage LESE responsibilities. Integrated HSE will look favourably on its HSE “returns”; its challenge might be to demonstrate cost-savings of prevented incidents to parts of the business.

HSE Excellence or Leadership—both costly endeavours—necessitates organisations to have become expert at identifying and preventatively addressing major HSE risks and opportunities. Differentiated HSE might appear to have a negative return on investment but, if successful, will realise added value in other aspects of the business—for example reputation, brand value, share price.

Area (A) beneath curve (i) represents the relative total business operating cost of HSE for each Type.

Area (A) beneath curve (i) represents the relative total business operating cost of HSE for each Type.

Immediately above this, the white-and-grey space (B) between lines (i) and (iii) represents the return on investment (or, more accurately, the avoided cost-to-company). This is negative in B1–meaning not only is HSE defective, but the company is counting pennies at the cost of pounds. The irony is that the business doesn’t view it this way because it has no idea what its true direct or indirect HSE costs are.

One definition of effective HSE might be when its operating cost is less than the true cost of actual-plus-prevented incidents (B2). The obvious challenge—but not insurmountable—is accounting financially for prevented incidents and thus being able to show this as a business-tangible benefit.

Finally, area (C) between lines (ii) and (iii) shows the volume of identified HSE liabilities. Put another way, everything beneath (iii) represents unidentified HSE liabilities. The larger this is, the greater the likelihood of unanticipated business interruption and compounded costs. This poses the question: can any business truly afford something less than effective integrated HSE?

The economics behind HSE is just one of its LESE business drivers—the others being legal, social and ethical factors. Economic and legal factors tend to be more visible and tangible to the business and its financial performance. Companies with defective HSE, or example, view social and ethical HSE risk control only as a cost—not as cost control. (This approach doesn’t make these risks go away.)

Therefore, just as a business’ economic priorities will consciously or unconsciously steer the organisation towards a particular HSE Type, so too will its LESE priorities. The importance of these less-tangible drivers will be based largely on senior management’s bias and stated views—the reason why HSE in general cannot succeed without visible top-level support.

In order to assess how HSE Types prioritise differently their “LESE” HSE risks and opportunities, it is useful to slightly expand upon them…

The legal, economic, social and ethical business drivers for HSE can be (slightly) expanded to financial, legal, operational, reputational, ethical, and social. Examples of each include:

Financial: government fines, cost-to-company such as insurance premiums or injury pay-outs

Legal: site closure, loss of operating permit or license, new or amended laws, imprisonment

Operational: interruption of profitable activities due to floods and no flood defence strategy

Reputational: brand value, share value, investor confidence, consumer loyalty

Ethical: doing something even though it costs money because it is the right thing to do

Social: community water contamination, wider regional air quality impacts, global climate change

The financial, legal, operational, reputational, ethical and social “LESE” issues outlined above can be now overlaid on the HSE Types model in the same way as for cost and liabilities.

The financial, legal, operational, reputational, ethical and social “LESE” issues outlined above can be now overlaid on the HSE Types model in the same way as for cost and liabilities.

With respect to the graph, right:

Lip Service HSE will be overly focused on financial considerations, albeit with legal requirements a secondary business factor when they become unavoidable—such as imminent threat of company fines, closure or even imprisonment. There will be no awareness or consideration of other LESE factors.

Compliant HSE remains focused on financial decisions, although legal compliance is clearly also important. Legal drivers, however, will likely remain secondary to financial ones for the same reason why this HSE Type is still defective: HSE is viewed as a cost-to-company and legal compliance can be expensive. There will be no awareness or consideration of other LESE factors because these are not business priorities.

Systems HSE will factor financial and legal decisions equally given that the latter is a type of system (along with ISO:14001, OHSAS:18001 and others). The company will be aware of and may occasionally act on reputational HSE risks, however, this is more likely to be a secondary outcome of a project than its primary motivator. There may also be awareness of ethical and social factors, although it’s probable these are viewed as one and the same thing.

Integrated HSE is aware of all HSE business considerations but with different priorities. Finances, operational continuity, and legal compliance remain primary drivers—despite the organisation very likely exceeding legal “minimum requirements”. Exceptionally strong motivation for reputational and ethical/social projects or programmes may be needed for management sign-off.

HSE Excellence factors all decisions in day-to-day business. However, social, economic, and operations are likely to remain dominant. Legal and reputational considerations carry weight but neither are the focus because the former is readily achieved and exceeded, and the latter is not the business’ primary HSE consideration (because that would change the HSE Type).

HSE Leadership recognises considerable reputational value in its HSE management and performance, followed closely by operational, social, and economic drivers. Legal requirements are exceeded by company standards. Financial factors play a part but, by the very nature of this Type’s focus on reputational value (with its own returns), cost is seldom a barrier to HSE leadership projects or programmes that maintain these organisations as topmost performers in their sectors.

HSE Types differentiate how businesses recognise, evaluate, prioritise and action their HSE risks and opportunities. Businesses and their key stakeholders can and should determine their preferred HSE Type and then build the HSE strategy and mission around this. This has business and HSE benefits. Overlooking this step can result in barriers or delays to HSE success, resulting in cost-to-company.

Even if a company doesn’t consciously select its HSE Type, however, it will still be determinable based on the organisation’s—its leadership and key stakeholders’ especially—HSE and related-LESE bias. This supports the long-standing view that the organisation’s culture—and especially that of its leadership—is critical to, and affects its HSE behaviours and performance. The dominant HSE and related LESE bias will inevitably drive a business to a specific HSE Type.

In targeting a higher Type, organisations will very likely have to overcome “barrier” behaviours including a failure to recognise, or a tendency to de-prioritise less-tangible LESE considerations. This is made harder and with considerable wasted time and resources by not honestly determining an HSE Type which the business then fully commits itself to achieving.

What do you think of the HSE Types concept and implications? Does this match your HSE experience? Are there gaps in the theory?

Your comments are most welcome.

Photo credits: wildpixel via istockphoto.com.

© Nick Hart (2017) All rights reserved. #hsetypes